FRANKFURT/LONDON/NEW YORK, Feb 24 (Reuters) – Financial firms from Frankfurt to Wall Street suffered heavy share price falls on Thursday as they grappled with the impact of Russia’s invasion of Ukraine, sought to understand what sanctions would look like and rushed to advise clients on how to respond.

While many bankers have played down the importance of Russia to their operations, it is the European Union’s fifth-largest trading partner, with a 5% share of trade, data shows. U.S. trade with Russia is less than 1% of its total.

Deutsche Bank (DBKGn.DE), Germany’s largest lender, said it had contingency plans in place as U.S. and European officials warned of further sanctions on Moscow. read more

Register now for FREE unlimited access to Reuters.com

Register

British bank Lloyds said it was on “heightened alert” for cyberattacks, while German insurance and asset management giant Allianz (ALVG.DE) said that it had frozen its Russian government bond exposure. read more

While U.S. banks were well-prepared for the measures announced so far over Russia’s aggression towards Ukraine, they worried that new measures could increase the cost and complexity of enforcing them. Financial institutions are the primary enforcers of sanctions. read more

“Anytime there is any type of financial strain across borders, financial companies particularly banks tend to be in the center of it because they have businesses in all those areas,” said Jamie Cox, managing partner at Harris Financial Group in Richmond, Virginia. “And their impacts are felt through currency fluctuations and things like that.”

Shares of leading banks plunged with the European banking sector (.SX7P) down 8% mid-afternoon, steeper than a 3.5% fall for the Euro Stoxx index (.STOXXE).

Top U.S. banks, including JPMorgan Chase (JPM.N), Citigroup (C.N), Goldman Sachs (GS.N), and Morgan Stanley (MS.N), shed 2-5%. That was a heavier fall than the broader market, with the S&P 500 (.SPX) down 1%.

Cox said banks were also being hit by U.S. Treasury yields declining. Investors piled into U.S. government debt and other safe-haven assets on Thursday after Russian forces moved into neighbouring Ukraine, pushing Treasury yields sharply lower. read more

“As you get Treasury yields falling, it has a deleterious effect on bank earnings,” Cox said. “So financial shares are getting hit from that side.”

Indeed, some of the region’s top bankers have been more concerned about the potential secondary effects of the crisis.

The boss of HSBC (HSBA.L), one of Europe’s largest banks, this week said that “wider contagion” for global markets was a concern, even if its direct exposure was limited. read more

Some banks organised calls for clients with experts to analyze the situation, invitations seen by Reuters showed, with JPMorgan scheduling one with Michael Singh, senior fellow at the Washington Institute for Near East Policy.

Goldman Sachs ran a call for its private wealth clients hosted by Alex Younger, a former chief of British foreign intelligence service MI6, who is now an employee of the firm.

CONTINGENCY PLANNING

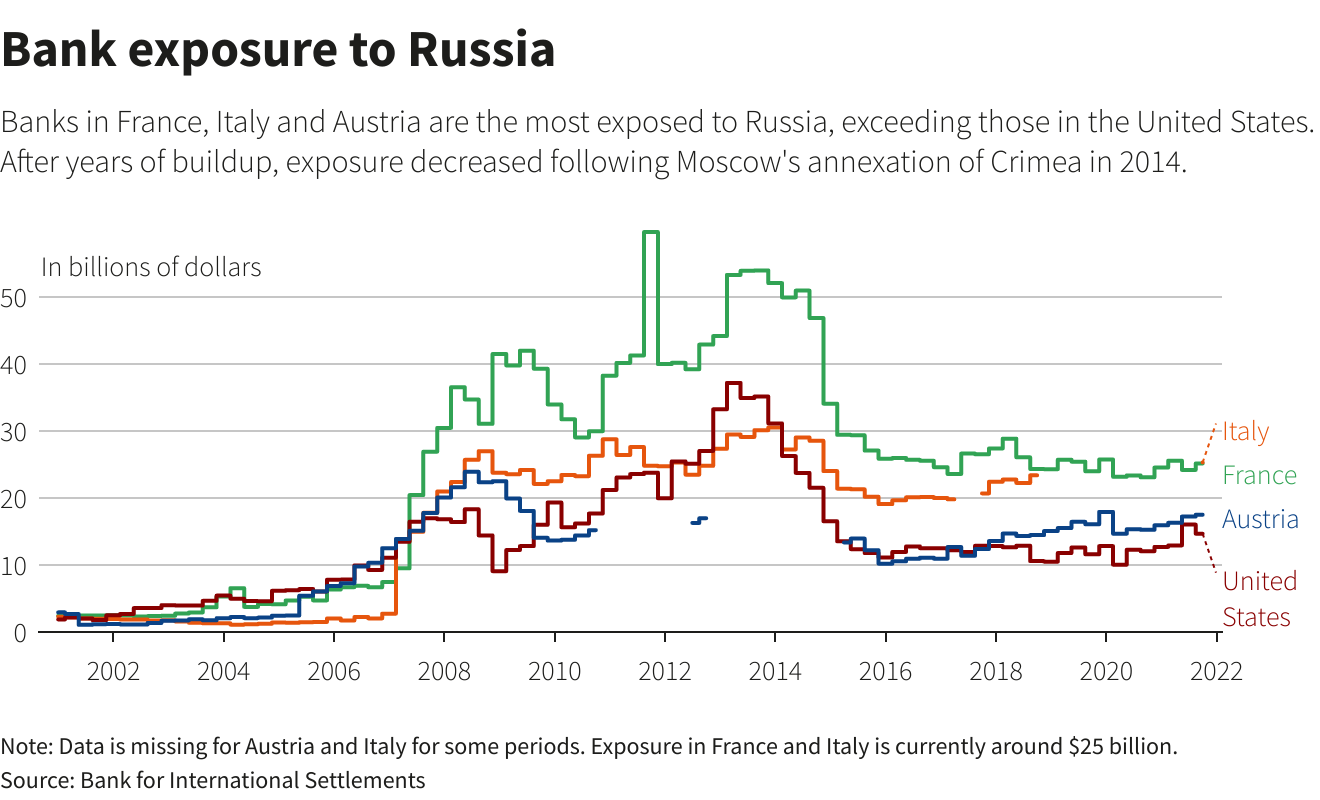

European banks are most exposed to Russia, especially in France, Italy and Germany, far outstripping U.S. banks’ exposure, data from the Bank for International Settlements shows.

And those banks with significant operations in Russia were hardest hit after its forces invaded Ukraine by land, air and sea, with the biggest attack by one state against another in Europe since World War Two. read more

Austria’s Raiffeisen Bank International (RBIV.VI) was down 19.5%, while shares in Societe Generale (SOGN.PA) lost 11.2%, although the French bank it said its Russian unit Rosbank continued to operate normally. read more

UniCredit (CRDI.MI) shares fell 12.4% and triggered an automatic trading suspension, although the Italian bank said its Russia “exposures are highly covered”.

Shares in Deutsche Bank, which like many lenders in recent years has reduced its presence in Russia as sanctions have expanded, were down more than 10.2%, the biggest decline among German blue chips.

“We have contingency plans in place,” the bank said in a statement. A spokesperson declined to elaborate, but said “risks are well contained”.

German financial regulator BaFin said it was keeping a watchful eye on the crisis.

FRESH SANCTIONS

European Union leaders will impose new sanctions on Russia, freezing its assets, halting access of its banks to the European financial market and targeting “Kremlin interests” over its “barbaric attack”, senior officials said. read more

But in what will be a relief to Europe’s banks, the EU is unlikely at this stage to take steps to cut off Russia from the SWIFT global interbank payments system, several EU sources said. read more

British Prime Minister Boris Johnson unveiled a package of “severe” sanctions against Russia on Thursday, targeting banks, members of President Vladimir Putin’s closest circle and the extremely wealthy who enjoy high-rolling London lifestyles. L8N2UZ366

Both Deutsche Bank and Allianz, two of Europe’s most important financial businesses and both with operations in Russia, said they were ready to comply with sanctions.

Allianz, one of the world’s biggest asset managers, said that the share of Russian government bonds in its portfolio was “very low” and that it had implemented a freeze on them.

RBI this month said it had earmarked 115 million euros ($129 million) in provisions for possible sanctions on Russia. As its shares dropped sharply on Thursday, the bank said that it was “premature to assess” the impact of sanctions on its business.

The Austrian group said its banks in Russia and Ukraine were “well capitalised and self-financing”.

U.S. Chamber of Commerce President and CEO Suzanne Clark said in a statement that Russia’s invasion of Ukraine was a serious breach of international law.

“The business community will continue to support the Administration, Congress, and our allies to ensure a swift and meaningful response to Russia’s aggression,” Clark said.

($1 = 0.8951 euros)

Register now for FREE unlimited access to Reuters.com

Register

Additional reporting by Alexandra Schwarz-Goerlich, Lawrence White, Valentina Za, Sujata Rao-Coverley, Kane Wu and Matt Scuffham, Devik Jain, Megan Davies; Editing by Tomasz Janowski, Jason Neely, David Goodman, Alexander Smith and Daniel Wallis

Our Standards: The Thomson Reuters Trust Principles.