Anyone hoping Libor’s death notice would accelerate the shift of hundreds of trillions of dollars worth of derivatives toward replacement benchmarks will be sorely disappointed.

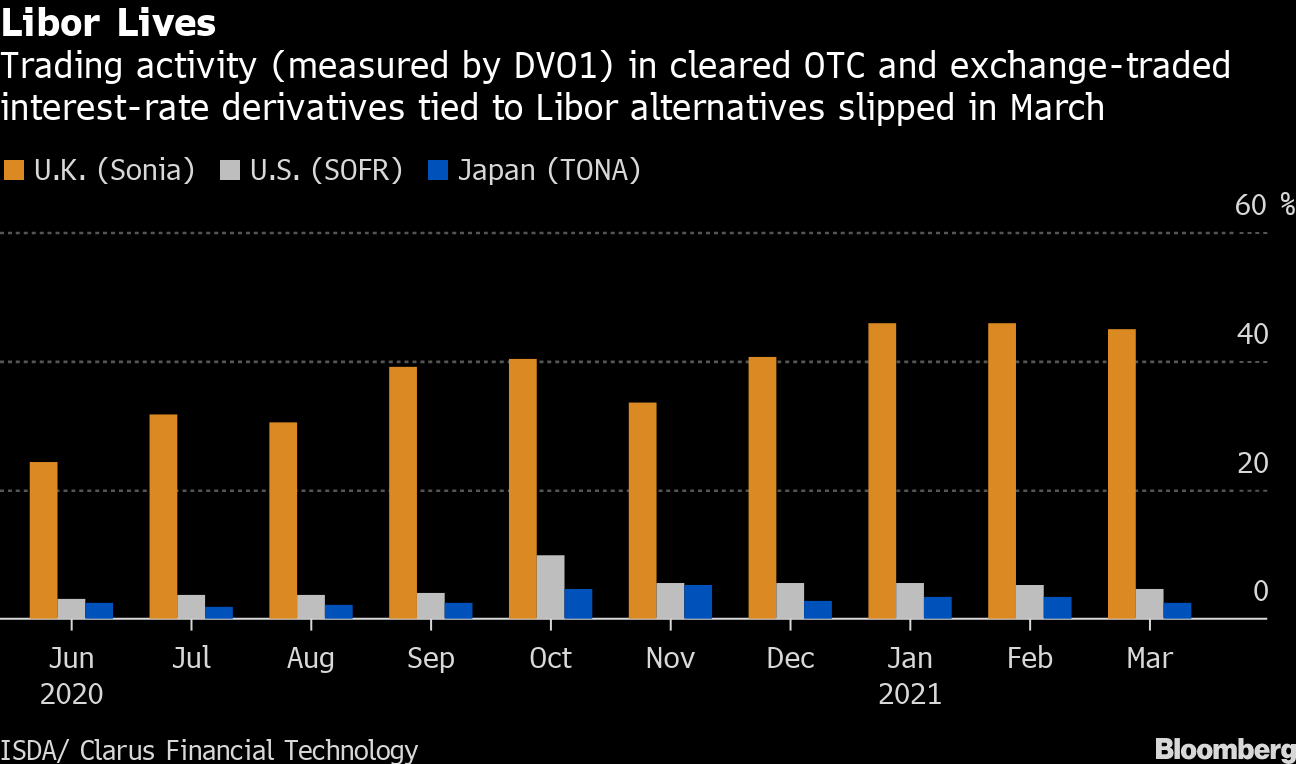

In the U.S, just 4.7% of contracts traded in March were pegged to the Secured Overnight Financing Rate, or SOFR, the benchmark slated to replace the London interbank offered rate, according to data from the International Swaps and Derivatives Association released Wednesday. That’s down from 5% in February.

Libor Lives

Trading activity (measured by DVO1) in cleared OTC and exchange-traded interest-rate derivatives tied to Libor alternatives slipped in March

ISDA/ Clarus Financial Technology

It’s a similar story in Japan, where 2.4% of activity was pegged to replacement rate TONA, the Tokyo overnight average rate, compared with 3.5% a month prior. Even in the U.K., where progress has been much more advanced, trading volumes linked to the Sterling Overnight Index Average, or Sonia, slipped to 45%, down from 46% the previous month.

In all these markets, most, if not all of the remaining activity is still linked to the London interbank offered rate. That’s even though global regulators confirmed last month that the final fixings for most rates tracking the benchmark will take place at end of this year. The key U.S. tenors will live on until mid-2023.

It shows just how entrenched the discredited Libor benchmark remains across global financial markets, despite efforts by regulators to drive it out for years following a manipulation scandal and a drying up of underlying trading data.

Read More: Libor Proving Hard to Kill in $200 Trillion Derivatives Market

“The volumes in SOFR are simply not there yet, and we cannot guarantee they will get there any time soon,” said ING strategist Padhraic Garvey.

The data vindicates the recent announcement by the Alternative Reference Rates Committee, the body guiding the U.S. transition, that it can’t guarantee a forward-looking term rate for SOFR by year-end due to insufficient liquidity, he said.

Analysts say that decision may help other Libor alternatives, such as Ameribor, ICE Benchmark Administration Ltd.’s ICE Bank Yield Index and Bloomberg’s Short-Term Bank Yield Index, to gather pace. The BSBY was created by the parent company of Bloomberg News.

“There are various bank indices now being given a new lease of life, as they do offer term rates,” Garvey said.

Still, the transition to SOFR could pick up from the end of June. That’s when firms should for the most part cease issuing new Libor-linked derivatives, according to best practice guidance from the ARRC.

Priya Misra, global head of interest-rate strategy at TD Securities and a member of the ARRC, said use will likely pick up from next year as cash products linked to the new rate increase.

“I don’t think the March indicator means people are giving up on SOFR,” she said. “It was just a high volatility month and that skewed the relative usage.”

Federal Reserve policy makers expect short-term interest rates will be pinned around zero for the foreseeable future, which may have contributed to the lackluster demand.

With SOFR fixed at 0.01% for the past month, floating-rate notes have become less alluring for investors like money-market funds, who are looking for assets that offer more yield.

(Adds reference to ICE Bank Yield Index, comment from ING, from eighth paragraph.)