What are derivatives?

Derivatives are contracts between two parties where the value of that contract derives from an underlying asset referenced by the contract. This explains why there is a lot of jargon around certain types of derivatives but once you break them down, most derivatives contracts are not particularly complex. For example, swaps are an agreement to exchange a series of future cash-flows over time which relate to a particular currency, interest or inflation rate.

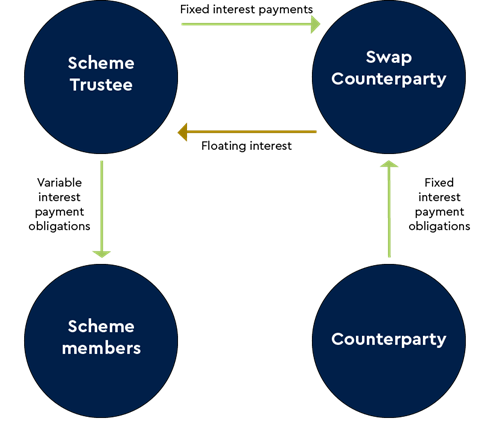

Interest rate swap

A scheme can hedge the risk of a rise in its variable interest rate payments to members, by agreeing to exchange interest rate payments with a counterparty who has fixed interest payment obligations. See diagram below.

The value of equity derivatives is related to the performance of particular stocks, indices, stock portfolios and exchange-traded funds. One example of this would be an equity forward, where one party agrees to sell and the other to buy particular shares on an agreed future date at a specific price (agreed in advance or determined by reference to a formula). On the maturity date the buyer can either expect to take physical delivery of the shares (‘physically settled’) or, depending on whether they are out-of-the-money, may receive payment (‘cash settled’). The amount paid is the net amount representing the difference between the market price of the shares at the relevant date and the agreed sale price.

As well as swaps and forwards, there are also options, swaptions, futures, credit derivatives, and many other more bespoke and exotic derivatives. The latter are more complex than more commonly-traded or simple ‘vanilla’ derivatives. Exotic derivatives will often have many triggers relating to how payments are calculated. For more, see our jargon buster.

Derivatives can be traded on an exchange or directly negotiated between parties. Generally, exchange-traded derivatives are for a term of one year or less, whereas OTC derivatives (private contracts between two parties which are not traded on an exchange) are usually longer term transactions. OTC derivatives make up around 90% of the London derivatives market.

Why use derivatives? Derivatives can be used by trustees of pension schemes as a flexible way to manage risk. Pension funds are asset-rich, so trustees can use derivatives as part of their investment management strategy to:

- facilitate efficient portfolio management (to assist risk and cost reduction);

- shape asset returns as part of a scheme’s liability driven investment strategy or cash-flow driven investment strategy (see below);

- reduce overall costs (using derivatives strategically to avoid using multiple products to achieve the same goal).

How can trustees use derivatives? Derivatives can form part of a scheme’s liability driven investment (LDI) policy. LDI is an investment strategy aimed at ensuring schemes have enough assets to satisfy their liabilities over the life of the scheme. The three main risks affecting a pension scheme’s liabilities are interest rates, inflation and longevity. As these liabilities can be volatile, an LDI strategy seeks to address this, matching investment asset returns to a scheme’s funding commitments.

Derivatives can form a key element in a scheme’s LDI strategy, as they provide:

- flexibility of investment,

- increased certainty that a scheme will achieve its objectives,

and can help to:

- reduce risk, and

- improve funding levels.

An LDI strategy can help a scheme improve investment returns as well as manage its liability risks. As swaps do not require an up-front allocation of assets (payments/exchanges are made in accordance with the swap terms), a scheme can make the swap payments as and when required whilst investing capital to assets elsewhere. This two-pronged approach (the reduction of risk whilst diversifying other asset investments) to generate growth helps to reduce funding level volatility.

The use of derivatives in LDI strategy need not be complex. A scheme can match its derivative investments to its long-term liabilities and enter into repos (repurchase agreements – see Jargon buster) alongside interest rate or inflation swaps, adjusting the allocation over time, as part of its LDI strategy.

Cashflow driven investment (CDI) can be used as part of an LDI strategy. CDI is a solution which matches future expected cashflow requirements of the scheme with contractual income from selected assets. CDI can be a useful strategy for better funded schemes, and requires minimal monitoring.