The International Swaps and Derivatives Association, Inc is the global trade association for OTC derivatives and maintains the industry standard documents for such transactions, namely the 2002 or 1992 Master Agreement, Schedule and credit support documents (the ISDA).

Unlike a company, which can contract directly with an ISDA counterparty, most DB pension schemes are set up as trusts, so the pension scheme itself has no legal personality. Instead, the ISDA is entered into by the trustee of the scheme as the legal owner of the scheme assets.

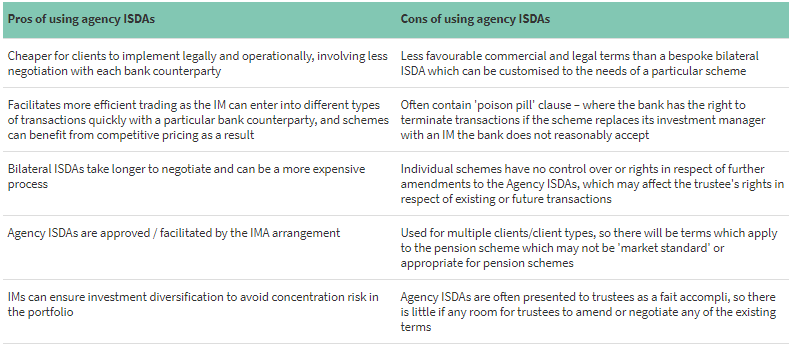

For many schemes, trustees will appoint an investment manager (IM) to manage their derivatives book. Although trustees can directly negotiate and enter into ISDAs, bespoke ISDAs are generally the preserve of larger pension schemes. More often than not, trustees will use ISDAs negotiated and agreed by their IMs under a kind of ‘umbrella ISDA’ with a particular counterparty bank, which is used by the IM to cover transactions it enters into on behalf of different stakeholders across its entire client book (known as Agency ISDAs).

Below is a summary of the advantages and disadvantages of using Agency ISDAs entered into by the IM on behalf of the trustee of a scheme, as opposed to bilateral ISDAs entered into directly by the trustee.

ISDAs – Key terms for pension schemes

Although the mechanics of the ISDA will generally facilitate the requirements of both parties, there are certain provisions which require amendment (via the ISDA Schedule) in order to reflect the particular characteristics of pension schemes.

- Insolvency events of default – the standard ISDA bankruptcy events of default are drafted to apply to companies. These should be disapplied for the trustee as they do not reflect how insolvency scenarios play out in the context of a pension scheme. Instead, pension scheme-specific insolvency events of default should be included in the ISDA.

- Other events of default – banks will usually insist on including pensions-specific default events to trigger their right to terminate transactions, e.g. where the scheme ceases to be a registered pension scheme under s.153 of the Finance Act 2004 or where the Pensions Regulator appoints a trustee to the scheme and as a result the original trustee (or IM on behalf of the trustee) is no longer able to perform any of its material obligations under the ISDA.

- PPF Additional Termination Event – ISDAs for pension schemes should incorporate the standard termination event language issued by the PPF dealing with pension schemes entering into the PPF. This will avoid a scenario where the occurrence of a particular event (e.g. an insolvency event in respect of the scheme’s sponsoring employer) triggers the bank’s right to terminate transactions under the ISDA, where commercially it would be beneficial for both parties for these transactions to continue. By way of example, where a pension scheme ISDA does not incorporate the PPF ATE wording; in a scenario where a scheme is transferred to the PPF, the bank counterparty would not have any comfort that the PPF would not exercise its statutory power to terminate or disapply provisions in the ISDA which disadvantage the scheme. Inclusion of the PPF ATE wording sets out the principles applied by the PPF when determining whether to exercise its powers, and increases legal certainty for both parties.