By Bitget CEO Sandra

Derivatives products have been playing a significant role in the global finance market. As the concept of decentralization experienced rapid development and gradually gained wider recognition among users in recent years, decentralized derivatives trading has naturally become one of the most promising markets. So is it possible for decentralized derivatives exchanges to disrupt their centralized counterparts in the short to medium term? Here are some of my thoughts and I’d like to share them with you.

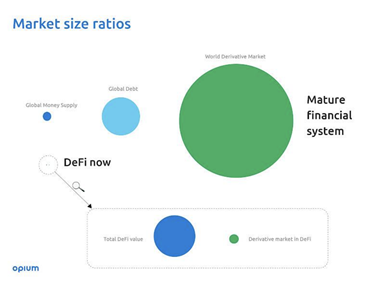

In the traditional financial sector, derivatives are classified into the following categories by different product forms: forwards, futures, options and swaps. Their underlying assets can be stocks, interest rates, currencies and commodities. The notional value of the overall derivatives market in 2020 is roughly $840 trillion, compared to $56 trillion for the equity market and $119 trillion for the bond market. And the size of the derivatives market is four to five times larger than that of its underlying assets.

While in the crypto world, most of the derivatives transactions happen in centralized exchanges in the forms of quarterly futures, perpetual futures (also called perpetual swaps) and options.

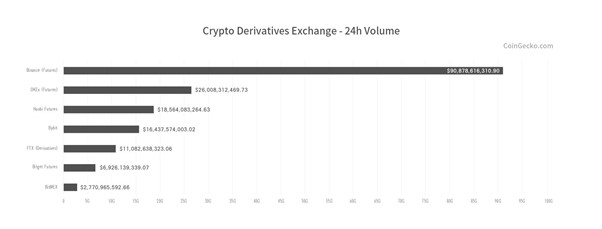

According to Coingecko, Binance, OKEx, Huobi, Bybit, FTX, Bitget and BitMEX are the world’s top7 derivatives exchanges. Take Binance as an example, its spot trading volume in the last 24h reached $23 billion while the derivatives trading volume hit $77.5, or 3.37 times the former.

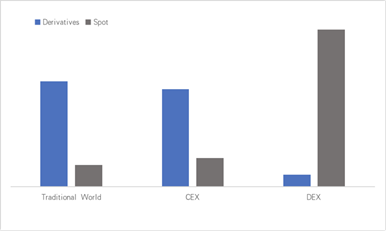

Things are quite different in decentralized exchanges (DEX). With a combined 24-hour trading volume of $1.25 billion for Uniswap V2 and V3 and $96 million for the decentralized derivatives exchange represented by Perpetual Protocol, futures trading volume accounts for only one-fourteenth of spot trading.

The world’s top7 derivatives exchanges. Source: Coingecko

The volume of derivatives trading vs. spot trading across different markets. Source: Foresight Ventures

Assuming that decentralized derivatives can also reach four times the volume of spot trading as in centralized exchanges, the room for growth is enormous. However, from what we see now, the business development of decentralized derivatives exchanges is far from satisfying.

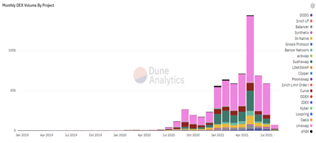

Trading data of decentralized derivatives exchanges. Source: Dune

Advantages and Disadvantages of Decentralized Derivatives Exchanges

In the decentralized world, there are mainly two types of derivatives: futures and options. Though index products, structured products and insurances are also derivatives, they are not the focus for our purpose here. Compared to centralized institutions in the crypto space, decentralized derivatives exchanges have the following advantages:

- Asset custody: The assets of decentralized derivatives projects are hosted on the chain. It is transparent and traceable, avoiding irregularities and default risks of centralized institutions.

- Fairness: Set by smart contracts in advance, the trading rules can not be tampered with in the back office, providing greater fairness for both parties to the transaction.

- Self-governance: In decentralized derivatives exchanges, things like the fees to be charged, coins to be listed and development plans can all be determined through community governance. People involved in the decision-making process could enjoy the benefits of project growth.

However, there are also urgent problems to be solved.

- Performance: Derivatives trading requires real-time transactions, which are difficult to achieve through the current on-chain solutions.

- Price discovery: Derivatives trading is extremely price-sensitive. However, the mark prices and transaction prices are dependent on the prediction of oracles.

- Risk control: Liquidation is a major issue for both decentralized and centralized exchanges. Decentralized platforms also need to address the on-chain congestion caused by extreme price volatility to ensure the liquidation process is reasonable and efficient, which is essential for the continued existence of derivatives platforms.

- Cost and liquidity: Margin trading with high leverages demands high liquidity of underlying assets. The platform needs to avoid the impact cost of transactions and establish a reasonable fee schedule.

- Capital utilization: a core requirement for traders to participate in derivatives trading is the ability to trade on margin with additional leverage, but the overcollateralization mechanism introduced by some synthetic asset projects once again limits the efficient use of capital.

- Anonymity: On-chain data are traceable, yet institutional investors want to keep their positions and futures contract address anonymous.

Different Types of Decentralized Derivatives Exchanges

In today’s market, decentralized futures derivatives have the largest number of project types and the most diverse solutions, mainly represented by perpetual futures, which currently fall into three major genres: AMM, order book and synthetic assets.

AMM represented by Perpetual Protocol

The AMM (Automated Market Making) based exchanges are mainly reinvented from the AMM model of Uniswap, such as vAMM and sAMM. It allows traders to interact with the assets in a physical or virtual asset pool to long or short.

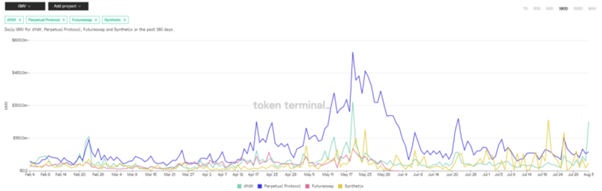

GMV Data of mainstream decentralized derivatives platform. Source: Token terminal

This type is mainly represented by Perpetual Protocol. According to Messari, Perpetual Protocol takes up 76% of the perpetual futures market and its revenue size in July was the seventh-largest of all Defi projects, behind Sushiswap. However, the trading volume and revenue do not accurately reflect its true market share as it is difficult to calculate how much is contributed by the wash trading resulted from the trans-fee mining initiated in February this year.

Based on a virtual liquidity pool called vAMM. The Perpetual Protocol uses the equation of X*Y=K to simulate pricing. Traders can input USDC as collateral to the Vault. So external liquidity providers are not required. It is also a way to mint synthetic assets. With the only USDC in the pool, there is no actual exchange between two actual currencies. The amount of funds flowing in and out of the Vault, as well as the returns, are calculated using a mathematical formula based on the price of the trading pair at the time of their entry and exit.

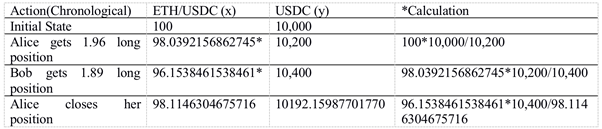

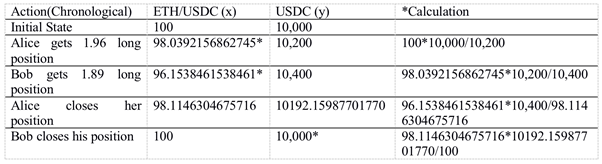

Let’s walk through an example trade explained by the project white paper.

- X*Y=K,The price ratio of ETH and USDC is Y/X=100

Assuming there are 10000 USDC in the Vault. X=100,K=100*10000. Alice uses 100 USDC as the margin to open a 2x leveraged long position on ETH;

- After that, the amount of USDC in the vAMMs will become 10,200 (10,000+100*2), the amount of ETH/USDC will become 98.04 (100*10,000/10,200), and the position Alices opens is 1.96 ETH (100-98.04).

- Following Alice, Bob also uses 100 USDC to open a long position with 2x leverage. His position size will be 1.89 ETH (98.03-96.15) using the same calculation. Note that the price of ETH increases due to Alice’s opening, therefore the average holding cost of Bob is higher than that of Alice.

- After Bob gets his long position, the price of ETH further climbs. Alice closes her position and realizes a profit of 7.84 USDC (10400 – 96.15*10,400/(96.15+1.96)- 200)

- Seeing Alice makes a profit, Bob wants to close his position too, only to find out that he lost -7.84 USDC (10192.15-98.11 * 10192.15 / (98.11+ 1.88)-200) after closing his position.

From the above example, we can see that one trader’s gain equals another trader’s loss. All traders in the pool are counterparties with their revenues calculated based on the virtual AMM model. This model has the following features:

- AMM model does not require the use of an external Oracle for price discovery. Instead, the price will reach equilibrium through the balanced activities of arbitrageurs between CEX and DEX. Though the approach can avoid the risk of Oracles, there could be an extreme deviation between asset prices in the exchange and outside market in the absence of arbitrageurs, leading to the liquidation of margin traders.

- In the Perpetual project, the K-value is a floating value set by the team. If the K-value is too small, the depth of the pool will be reduced. But if the value is too large, the price fluctuation in the exchange will be too minor to match the outside price. Therefore, the setting of the K value will significantly impact the operation of the AMM model.

- In the AMM model, large orders will incur greater impact costs to the pool, especially for price-sensitive futures traders, whose revenue will be significantly influenced by the size and sequence of the orders.

To address the above issues, Perpetual Protocol launched a V2 “Curie”. The major improvements include:

- It built Uniswap V3 into the original vAMM pool and created a liquidity pool in the form of v-token (such as vETH/vUSDC). When traders deposit USDC to open a position, the leverage liquidity provider will generate and input the amount equivalent to that of the position. This is also a way of minting synthetic assets. The only difference is that it uses a liquidity pool consisted of actual tokens to replace the original mathematic formulas.

- Introducing the role of makers to provide liquidity management for Uni V3 can improve its liquidity to some extent. But the liquidity of the pool depends on the funds and market-making capacity of the makers.

- The Insurance Fund could be used to cover abnormal settlements and serve as the counter-party when there is an imbalance between long and short positions to provide more liquidity to the pool.

It seems that the AMM solution used by Perpetual V1 can provide unlimited liquidity, but it will suffer from inevitable impact cost when a larger amount of funds is involved. The upgraded V2 model is also subject to the ability of makers. Liquidity providers who employ the active market-making strategy of Uni V3 may also bear the impermanent losses. Although the AMM model has tackled the long tail problem of the derivatives market, its impact cost is still high for large-scale and price-sensitive traders.

Order book model represented by dYdX

The locked amount and profit statistics of dYdX. Source: Token terminal

As one of the earliest trading platforms for decentralized derivatives, dYdX launched its first BTC-USDC perpetual futures last May. It went on to co-built a Layer 2 solution for cross margin perpetuals on the StarkEX engine together with StarkWare this April. Apart from supporting perpetuals, dYdX also offers lending, spot trading and margin trading. Its futures trading volume ranks second in the decentralized perpetuals market, accounting for 12%.

Adopting the order book model with Wintermute as its leading maker to provide liquidity, dYdX combines off-chain matching with on-chain settlements. Therefore, the transaction model is basically the same as CEX, with the transaction price determined by the market price, which is in turn set by the maker. According to data released by Wintermute, 95% of the current transactions on dYdX are quoted by makers, making them the core strength for order-book-based platforms. This is the reason why most critics criticize dYdX for being too centralized.

The order book model is very demanding on the performance of matching and transactions. It basically operates like this: StarkEX will obtain a sequence from dYdX, runs them internally, and ensures that everything is checked out and meaningful. Then, it moves the transaction to the Cairo program. The Cairo compiler will compile the Cairo program, and then the prover will convert it into a STARK proof. Then, the proof will be sent on this chain to the verifier for verification. The proof is legal if it is accepted by the verifier. So everyone can check the account balance of all users on Layer 1 but the transaction data is not created on the chain. In this way, it protects the privacy of the transaction strategy and reduces transaction costs. At the same time, the gas fee on Layer2 will be borne by the dYdX team. Users only need to pay a transaction fee.

As Layer2 and other scaling solutions improve over time, the user experience of order-book transactions will very much resemble that of a DEX. In addition, more advanced orders have been launched by dYdX, including market orders, limit orders, Take profit and Stop loss, Good-Till-Date, Fill Or Kill or Post-Only, offering traders futures trading services that are increasingly similar to those of centralized exchanges. For a future exchange, there are different priorities at various stages. For example, relying solely on makers is a necessary approach to maintain liquidity in the early days. As professional investors entering the market, the entire ecosystem will evolve and become less centralized.

Synthetic assets model represented by Synthetix

The locked amount and profit statistics of Synthetix. Source: Token terminal

As the earliest and largest synthetic assets platform, the development of Synthetix is well known to most of the readers and will not be elaborated here. On Synthetix, users stake SNX to generate sUSD based on a collateralization ratio of 500%, and then exchange the sUSD into any synthetic assets within the system through transaction. They can go long on sToken, or go short on iToken. The assets to be transacted are not limited to cryptocurrencies, but include Forex, stock and commodities. In our discussion, synthetic asset is listed as one of the transaction models for decentralized derivatives because it is also a kind of futures contract traded with collateral, or margin.

The transaction model of SNX is fairly new in that it introduces the concept of a “dynamic debt pool”. The debt borne by the users and the system will change in real-time. When a user stake SNX to mint sUSD, the sUSD becomes the debt of the system. When the users convert the sUSD into sToken, the debt of the system will evolve as the value of the sToken changes. And such debt is shared proportionately by all users who have staked SNX. Let’s look at an example:

Suppose there are only A and B in the system. They each minted 100 sUSD.

| A’s debt | B’s debt | Total debt | |

| Mint 100 sUSD | 100 sUSD | 100 sUSD | 200 sUSD |

| A uses them to buy sBTC; B holds them | 100 sUSD | 100 sUSD | 200 sUSD |

| BTC price doubles(before debt distribution) | 200 sUSD | 100 sUSD | 300 sUSD |

| BTC price doubles(after debt distribution) | 150 sUSD | 150 sUSD | 300 sUSD |

Eventually, their debts are both 150 sUSD, but A’s asset value reached 200 sUSD while B’s asset remained 100 sUSD. At this point, if A sells sBTC to get 200 sUSD, then he will only need 150 sUSD to redeem SNX, while B will need to buy 50 sUSD before redemption.

From this point of view, Synthetix’s debt pool model is actually a dynamic zero-sum game. The profit may come from the rise in the price of one’s own assets, or the fall in the price of other people’s assets; vice versa. Or we can say, stakers on Synthetix are actually going long on “their own investment capability/the investment capability of other participants” You may also hold sUSD in the long term, but this will put you at the risk of “I may lose money because other investors are too capable.” As Taleb says, by staking SNX to generate sUSD, users have skin in the game. The bold design of risk-sharing turn all users into real “stakeholders”.

Source: Mint Ventures https://www.chainnews.com/articles/894865830615.htm

This bold and creative design of SNX is essentially similar to the zero-sum game built in the AMM model. And for vAMM, its process of inputting virtual assets as per the amount of open positions also resembles the minting of synthetic assets. The difference is that Synthetix, fed by an oracle machine, does not have to worry about price slippage or the flow of assets. In this way, it provides the users with truly unlimited liquidity.

Current Problems for Decentralized Derivatives Exchanges

After illustrating on how decentralized derivatives products operate, let’s get back to the problems listed at the beginning of this article. Can they be solved by the above projects? What’s the future of decentralized derivatives products?

Performance

The performance issues are now being partly addressed, with various decentralized derivatives platforms adopting different scaling options: Perpetual Protocol uses the sidechain solution xDai; dYdX adopts Layer2 solution based on ZK-rollup technology to conduct off-chain matching and on-chain record-keeping; SNX implements a Layer2 scaling solution “Optimisitc”. These scaling solutions have addressed the demand for real-time transaction and the front-run problem during transaction execution.

Price Discovery

For the AMM model, prices are mainly defined by assets within the pool and the equation of x*y=k. The execution price is independent from an external oracle, but the funding fee uses Chainlink’s price feed as the index price. The Perpetual V2 also will combine Uniswap oracle after introducing the liquidity pool of Uni V3. The AMM model is therefore less susceptible to oracle failures.

On dYdX, three different prices are used: index price, oracle price and mid-market price. Among them, the index price is maintained by the dYdX team. It is determined by referencing the prices of 6-7 spot exchanges and is used to trigger conditional orders. The oracle price is provided by Chainlink and MakerDao for the calculation of margins and funding fees. The mid-market price is the price generated by the order book, also used to calculate the funding fees. The price discovery model of dYdX is similar to CEX where the execution price is based on the order book while liquidation price is determined by the oracle. On the whole, the price of dYdX is mainly influenced by makers and arbitrageurs, but its liquidation price may be affected by the risks of oracle malfunction.

In comparison, SNX uses Chainlink decentralized oracles to power all price feed on its platform, including the transaction price, system debt and liquidation price.

Risk Control

We can see that almost all derivatives exchanges rely on oracle prices for liquidation, which occurs when the position margin ratio falls to a certain level. In such cases, the users will be compensated through the mechanism of Insurance Fund. Given that most of the projects are dependent on the quotes of Chainlink, the risk of oracle attack seems to be unavoidable. Moreover, the on-chain liquidation congestion problem caused by violent price swings remains unsolved, yet it may be mitigated through scaling solutions in the future.

Cost and Liquidity

The problem is twofold: small volume traders need to bear higher gas fees, and large volume traders have to pay higher impact costs caused by liquidity. While the former has been partly resolved through Layer2 solutions, the latter is more complex. It can be quite difficult to dodge in the AMM model; for platforms based on order books, it may depend on the market-making capacity and capital size of the makers; for synthetic assets, the impact cost of a single trader may be smoothed out if the capital size of the overall protocol is large enough.

In addition, transaction fees can be another concern for derivatives traders with a higher turnover rate. From the current statistics, the transaction fees of DEXes are much higher than those of CEXes. For example, Perpetual Protocol charges 0.1% for each transaction, while dYdX collects a maker fee of 0.05% and a taker fee of 0.2% for ordinary users, compared to 0.02%-0.04% in centralized exchanges. Even though all the above projects have launched the trans-fee mining feature to compensate the transaction fees, the final transaction cost in DEXes is still relatively high.

Capital Utilization

In terms of capital utilization, the DEXes based on AMM and order books are not very different from CEXes. The maintenance margin ratio is 6.25% for Perpetual Protocol and 7.5% for dYdX. But derivatives exchanges based on synthetic assets, such as SNX, require a 200% overcollaterization to avoid liquidation. Though SNX can provide unlimited liquidity, the overcollaterization mechanism puts significant restrictions on capital utilization, which goes against the intention of futures trading.

Anonymity

The current scaling solutions of all exchanges are moving most of the transaction data to off-chain. Take dYdX for example, it uses “zero-knowledge proof” to protect the privacy of users. It can be expected that the anonymity of futures will be guaranteed as privacy-focused layer2 solutions improve over time.

Conclusion

From the above comparison between decentralized derivatives exchanges, we can see that the order-book platforms represented by dYdX can better solve the major pain points of currents derivatives products. Their transaction models and functions are also more in line with the habits and needs of derivatives traders. Critics may accuse dYdX of not being decentralized enough, but actually, it is just a strategic choice between survival and development at different stages. After all, the primary goal of a decentralized project is to meet the basic needs of users, while decentralization could be gradually achieved by engaging more institutions and diversified participants to enhance the ecosystem.

Like fresh produce in e-commerce faced with various limitations in products, technology, and channels, derivatives also find it challenging to break barriers. It is therefore not likely for decentralized derivatives exchanges to shake up the dominant position of CEXes. However, with the development of Layer2 and other scaling solutions, their problems regarding performance, risk control, transaction cost and anonymity will be partially solved. It is fair to say decentralized derivatives exchanges will become the biggest beneficiary of Layer2 technology. From a long-term perspective, derivatives trading is still one of the most promising segments with unlimited possibilities.